Postgraduate Repayment Thresholds: Lack of a Rise Could be a Real Downer

The Government has confirmed that the 6 April 2018 rise in student loan repayment thresholds won't apply to postgraduate loans. This is surprising and disappointing.

If we know one thing about the postgraduate loans introduced from 2016, it’s that the system has been successful: at least in terms of attracting students, with full-time enrollments up by roughly 22% for 16-17.

And, if we know one thing about those students, it’s that they’re increasingly conscious of the cost of their degrees – and the loans that finance them.

This lies behind the Government’s recent decision to raise the repayment threshold for undergraduate student loans, from £21,000 to £25,000.

Yet it also lay behind the earlier decision to introduce a slightly different repayment system for Masters loans. Responding to concerns about concurrent undergraduate and postgraduate repayments, the Government lowered the rate at which the latter are made (from 9% to 6%).

Based on the available data, it seems like this relatively minor adjustment has worked: students seem willing to accept a PGL system that, rather than dramatically increasing their repayments, simply adds an additional, relatively small, deduction.

The problem is that this is no longer the case, as the Government has confirmed that the threshold rise won't apply to Masters loans.

So, for a (post)graduate earning between £21,000 and £25,000, that 6% deduction is no longer additional, or relatively small.

Instead, taking on a PGL effectively means opting in to earlier repayments. Or, to put it another way, a graduate who decides to take on a Master's degree and fund it with a Master's loan, is effectively opting out of a widely-publicised policy change designed to benefit them. Their peers will be repayment-free until they earn over £25,000. They won't be.

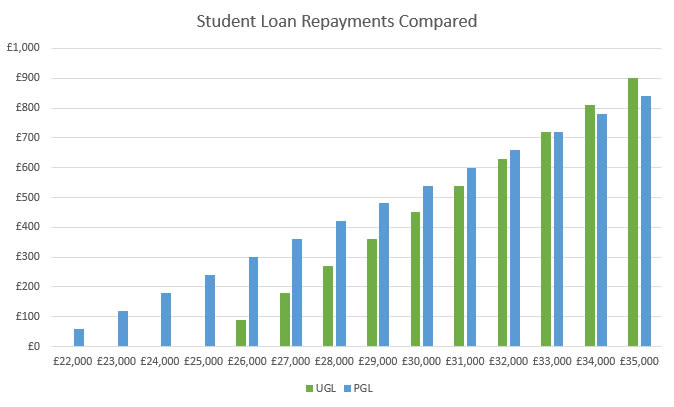

The psychological impact of this on prospective students remains to be seen. The financial impact looks like this:

Despite the lower rate of deduction, PGL repayment is now more expensive than UGL repayment until a graduate earns over £33,000.

To some extent, this is all a matter of perspective: after all, the PGL hasn't actually become any more expensive. But has the Government just managed to make it less attractive, nonetheless?